Healthcare Costs and the Hidden Driver of Food Insecurity

February 20, 2026

I spent most of my career on the other side of health insurance. Advising employers on benefits strategy and compliance. Helping organizations navigate the complexity of coverage design.

This year, for the first time, I was the one shopping the ACA marketplace, after my COBRA coverage expired.

It was a clarifying experience. And it got me thinking about something I work on every day at FastRoots: food insecurity.

The connection that does not get enough attention

Food insecurity is fundamentally a resource allocation problem. Families facing hunger are not making poor choices; they are making impossible ones. When fixed household income has to stretch further to cover one basic need, something else gets cut. Usually food.

The expiration of enhanced ACA subsidies at the end of 2025 is exactly this kind of pressure, and the numbers are larger than most people realize.

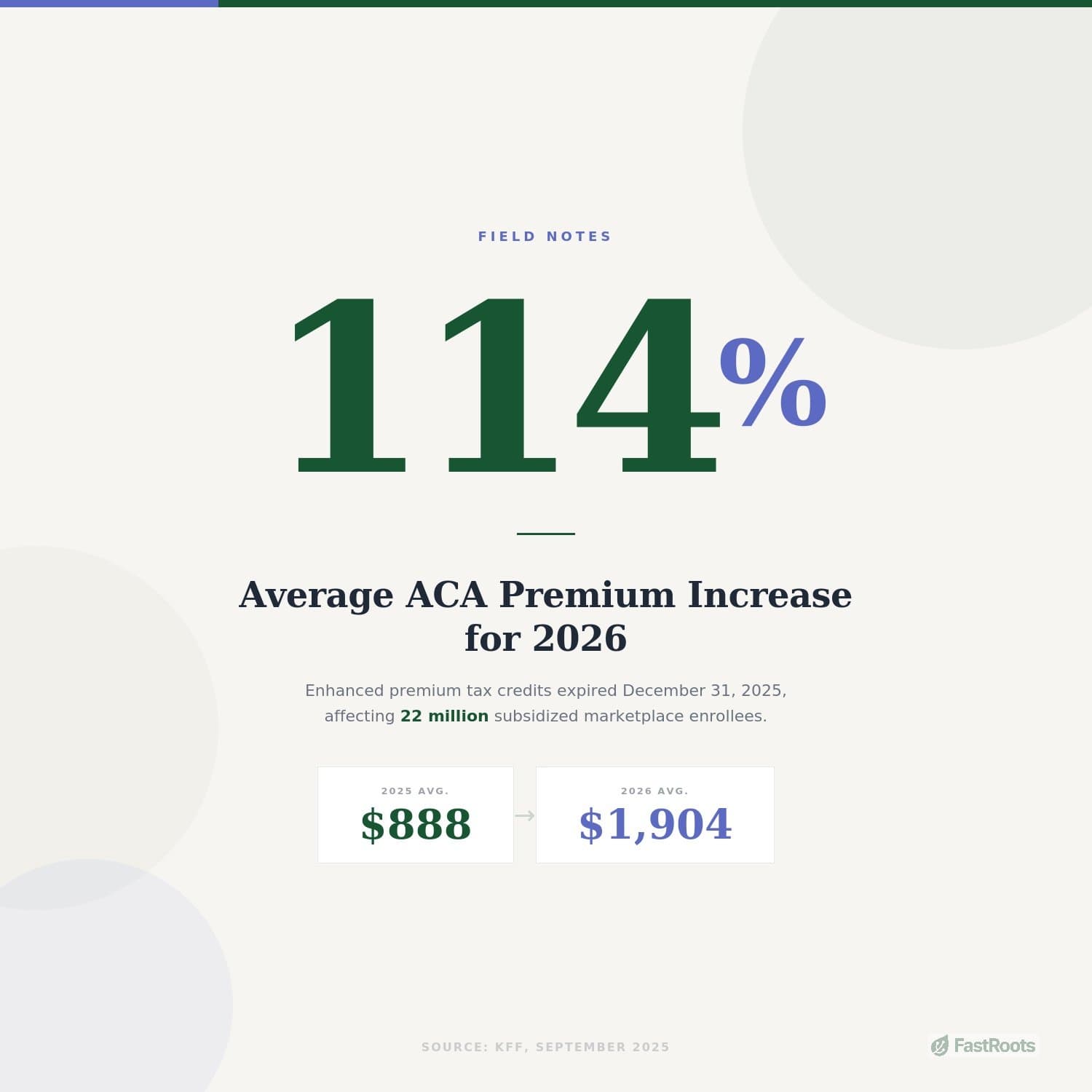

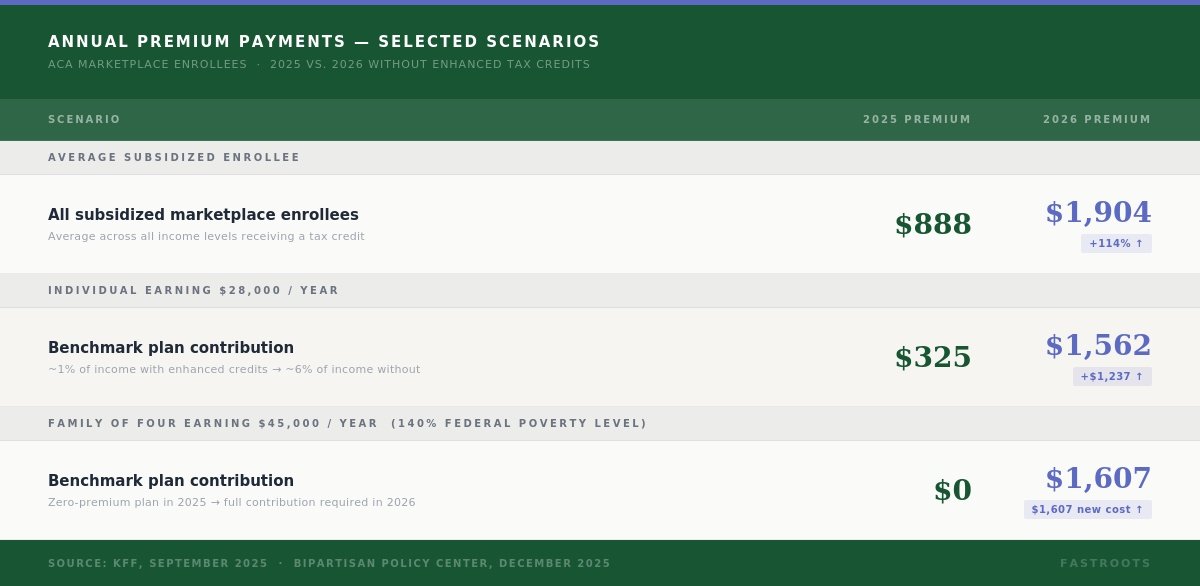

According to KFF, the expiration of enhanced premium tax credits is estimated to more than double what subsidized enrollees currently pay annually, a 114% increase from an average of $888 in 2025 to $1,904 in 2026. For an individual earning $28,000, annual premium contributions jump from $325 to $1,562. That is an extra $1,237 that has to come from somewhere.

For a family of four earning $45,000, the math is even starker. A family at that income level, which sat at 140% of the federal poverty level, paid $0 in premiums in 2025. In 2026 they will owe $1,607 per year. Bipartisan Policy Center

And for older enrollees approaching retirement, the cliff is steep. A 60-year-old earning $64,000, roughly 409% of the federal poverty level, would pay about $14,900 in annual premiums in 2026, representing more than 23% of their income. CNBC In 2025, that same person paid 8.5%.

That is not an abstraction. That is a grocery budget. That is a utility bill. That is the margin between stability and crisis for millions of households.

Roughly 14% of U.S. households reported food insecurity between January and October 2025, up from 12.5% in 2024. That increase happened before the subsidy expiration took effect. The households now absorbing ,200 to 4,000 in new annual healthcare costs are the same households already making tradeoffs between food, rent, and medicine.

The Urban Institute estimates that 4.8 million people will lose coverage entirely. When people lose coverage, they defer care, accumulate medical debt, and face financial shocks that ripple across every basic expense. The Capital Area Food Bank's 2025 Hunger Report found that 83% of food insecure households had drained savings to cover basic costs, up from 64% just two years prior. Healthcare premium increases do not arrive in isolation. They land on top of all of that.

Healthcare is a basic need. When we treat it as a market luxury subject to price swings, we create cascading shortfalls in every other basic need category.

What this means for foundations

This is where I want to speak directly to the foundation leaders reading this.

The conventional framing of food insecurity focuses on SNAP enrollment, pantry capacity, and meal counts. Those metrics matter. But they measure the symptom, not the system. The actual drivers of food insecurity are upstream: income volatility, housing costs, childcare costs, and yes, healthcare costs. When one of those upstream drivers spikes sharply, demand at food banks and meal programs follows within months, not years.

That lag matters. By the time premium increases translate into visible food pantry demand, the increase has already happened. Foundations that wait to see it in their grantee reports before adjusting their strategies are already behind.

There are three practical questions worth asking right now.

- Do you know how many households in your service area are currently enrolled in ACA marketplace plans? State health exchange data is public and can be mapped to county level. The states facing the steepest coverage losses, according to Becker's, tend to be in the South and Southeast, including the Carolinas, where many community foundations already carry significant food relief portfolios.

- Do your food relief grantees have capacity to absorb a demand increase? If the 2026 enrollment drop and premium shock play out as projected, local food programs will see more households for the first time, households that were previously covered and employed and not in crisis. Those are different clients than the chronically food insecure, and they often need different kinds of support.

- Is your foundation thinking about healthcare access as a food security issue? The two are tightly linked in the research. There is a bidirectional relationship: food insecurity worsens health and increases healthcare costs, while poor health and attendant medical expenses deepen food insecurity by reducing the ability to work and increasing household debt. CDC Foundations that hold both lenses simultaneously are better positioned to fund interventions that actually interrupt the cycle.

Healthcare is a basic need

I believe that not as a political statement, but as a practical observation. When we treat it as a market luxury subject to price swings, we create cascading shortfalls in every other basic need category.

The policy conversation happening in Washington is not abstract budget math. It is a direct upstream driver of food insecurity at the local level. Community foundations, food banks, and local nonprofits will feel this in their demand numbers, and many already are.

Those of us working in food relief need to be paying attention.